Most Stock Markets Go Up Most of the Time

Including during World Wars and COVID-19 Most stock markets go up most of the time.

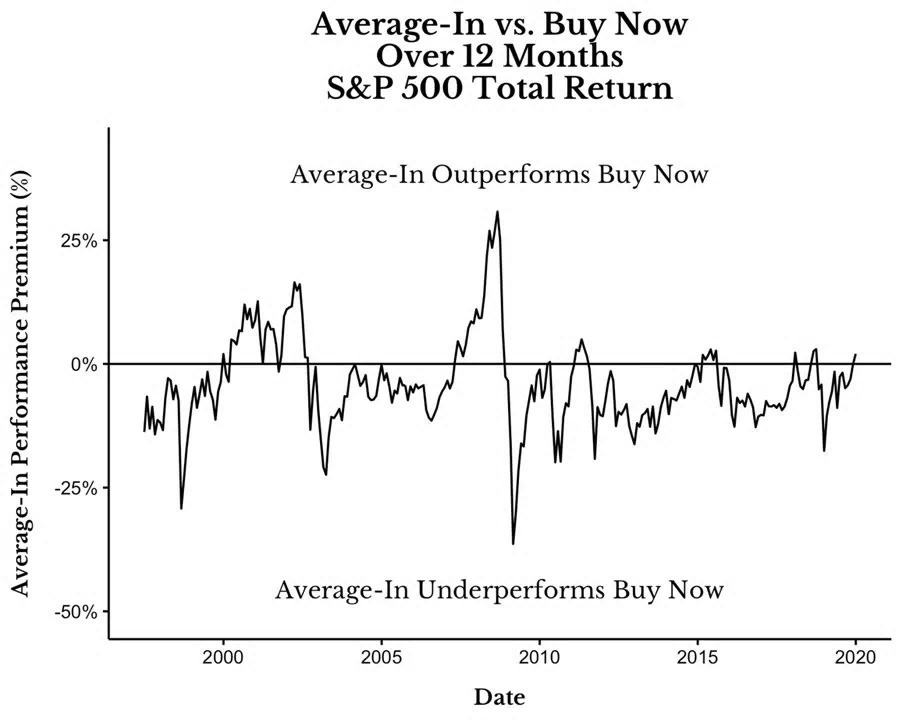

While it feels like we are always at the epicenter of a market crash, the fact is that major crashes are very rare. This is why Average-In has performed poorly for most of history.

The Best Time to Start Was Yesterday

The next best time is today. The best time to start was yesterday. The next best time is today.

- If we assume that the assets you are investing in will increase in value over time (otherwise why would you be investing?), then it should be clear that buying now will be better than buying over the course of 100 years. Waiting a century to get invested means buying at ever higher prices while your uninvested cash also loses value to inflation.

- If we assume that the assets you are investing in will increase in value over time (otherwise why would you be investing?), then it should be clear that buying now will be better than buying over the course of 100 years. Waiting a century to get invested means buying at ever higher prices while your uninvested cash also loses value to inflation.

Why There Might Be Better Prices in the Future

One trading day out of every 20 (one per month) will offer you an absolutely cheap price. The other 19 will leave you regretting your purchase at some point in the future. This is why it feels right to wait for lower prices. Technically, you have a 95% chance of being right.

Why You Shouldn’t Wait

Sometimes lower prices never appear, or you might have to wait a very long time to see that lower price. The most critical point is that you cannot time the market; you don’t know when the price will be better. Because “better” is a relative concept.

While it feels like we are always at the epicenter of a market crash, the fact is that major crashes are very rare. This is why Average-In has performed poorly for most of history.

Why did “Buy Now” perform so poorly compared to Average-In in August 2008?

Why did “Buy Now” perform so poorly compared to Average-In in August 2008?

Because the US stock market crashed shortly after August 2008. More specifically, if you invested $12,000 in the S&P 500 index at the end of August 2008, by the end of August 2009, you would only have $9,810 (including reinvested dividends), resulting in a total loss of 18.25%.

However, what you truly see in this chart is not the peak, but the line usually being below 0%. If the line is below 0%, Average-In performs worse than Buy Now, and when it is above 0%, Average-In performs better than Buy Now.

As you can see, most of the time, Average-In performs worse than Buy Now. This is not just recency bias. If we look at US stock returns since 1920, we find that in every rolling 12-month period, the average performance is 4.5% lower than “Buy Now,” and across all rolling 12-month periods, the average performance is 4.5% lower than “Buy Now.” The chart below illustrates this longer period in the same way as the previous chart.

What About Risk?

High returns inevitably bring high risk. Is it worth risking a larger drawdown for a potential 4% gain?

However, if you are worried about risk, then maybe you should consider following the Buy Now strategy and investing into a more conservative portfolio instead.

For example, if originally you were going to Average-In to a 100% stock portfolio, you could follow the Buy Now strategy into a 60/40 stock/bond portfolio to have slightly better returns for the same level of risk.

If you think that the market is overvalued and due for a major pullback, you may need to wait years, if ever, before you are vindicated. Consider this before you use valuation as an excuse to stay in cash.

Final Summary

When deciding whether to invest all funds now or invest over time, investing now is almost always better. This applies to all asset classes, time periods, and almost all valuation regimes. Generally speaking, the longer you wait to deploy your funds, the worse your situation will be.

The reason I say this is that over time, the only time you can improve by averaging in is when the market crashes. However, precisely when the market crashes, you are least inclined to invest.

Everyone is frantically selling, and you don’t know how far the market will fall.

It is hard to resist these emotions, which is why many investors cannot continue buying when the market is falling.

AI Q&A

The author’s core view is: stock markets go up most of the time, so investing early is better than diversifying, because waiting usually means missing out on upward opportunities. Historical data shows that the average cost method performs worse than lump-sum investing most of the time (76% to 82% of 12-month periods), especially when the market is generally trending upward. Even if lower prices might appear in the short term, the long-term gains from entering the market early are greater.

Validity of the Author’s Argument

Data Support

- The author provides sufficient historical data to support the argument.

- Analysis across multiple asset classes and time periods shows that lump-sum buying indeed yields higher average returns.

- Even during periods of high valuation, lump-sum buying is statistically superior.

Theoretical Basis

- The long-term upward trend of the market indeed supports the logic of investing early.

- Adjusting asset allocation to control risk is a reasonable suggestion.

Limitations of the Author’s Argument

Psychological Factors Not Fully Considered

- Investment decisions are not just mathematical and statistical issues.

- The psychological pressure of investing a large sum upfront may lead investors to make poor decisions during market downturns.

- One of the values of dollar-cost averaging (DCA) is helping investors build good investment habits and psychological resilience.

Differences in Individual Circumstances

- Different investors have different risk tolerances.

- The stability of income sources affects the choice of investment strategy.

- Differences in investment goals and time horizons should also be considered.

Real-world Complexity

- The real market environment is more complex than historical data.

- Factors such as macroeconomic conditions and policy changes can affect strategy performance.

- Past performance cannot fully predict the future.

Suggested Balanced Viewpoint

Strategy Combination

- One can consider combining lump-sum buying and dollar-cost averaging (DCA).

- For example, investing a portion of funds upfront while maintaining a regular investment habit.

- This way, you can gain the advantages of early investment while maintaining investment discipline.

Tailored to the Individual

- Choose the appropriate strategy based on specific individual circumstances.

- Consider your risk tolerance, investment experience, and financial goals.

- Choosing a method that allows you peace of mind is more important.

Dynamic Adjustment

- Regularly evaluate and adjust the investment strategy.

- Make appropriate adjustments based on changes in market conditions and personal circumstances.

- Maintain flexibility and adaptability.

Conclusion

The author’s analysis is convincing from a data and theoretical perspective, but investment decisions should not be based solely on historical data. Every investor needs to find a method that suits them, balancing rational analysis with psychological endurance. While DCA might be slightly inferior in terms of pure returns, its value in reducing psychological pressure and cultivating investment habits should not be overlooked.