More than huge returns, the safety of wealth is paramount.

- Extreme success largely depends on luck.

- Investing and wealth management isn’t entirely based on luck. It might be a bit like playing cards—there’s a significant element of luck, but also a certain level of skill.

- Personal financial investment is largely related to psychology.

- Investment behavior is strongly related to a person’s past experiences, because past experiences influence one’s psychology.

Chapter 1: No One Truly Loses Their Mind Over Money

In the United States, the lowest-income families spend an average of $412 annually on lottery tickets, which is four times the amount spent by high-income families. 40% of Americans cannot pull out even $400 when they urgently need money. This means that those who spend $400 on lottery tickets are essentially those who cannot produce $400 when they need it most. They are betting the $400 that could provide them with security on a chance of winning that is only one in a million.

Few people make financial decisions simply based on electronic reports. Decisions are often made while people are dining or in meetings. In these settings, personal experience, unique worldview, subjective self, pride, marketing tactics, and extraordinary incentives all work together to form the context that prompts you to make a decision.

The 401K plan—America’s main retirement system—only appeared in 1978; the Roth IRA was born in 1998. If we view the latter as a person, he has just reached the age of legal drinking.

Chapter 2: Luck and Risk

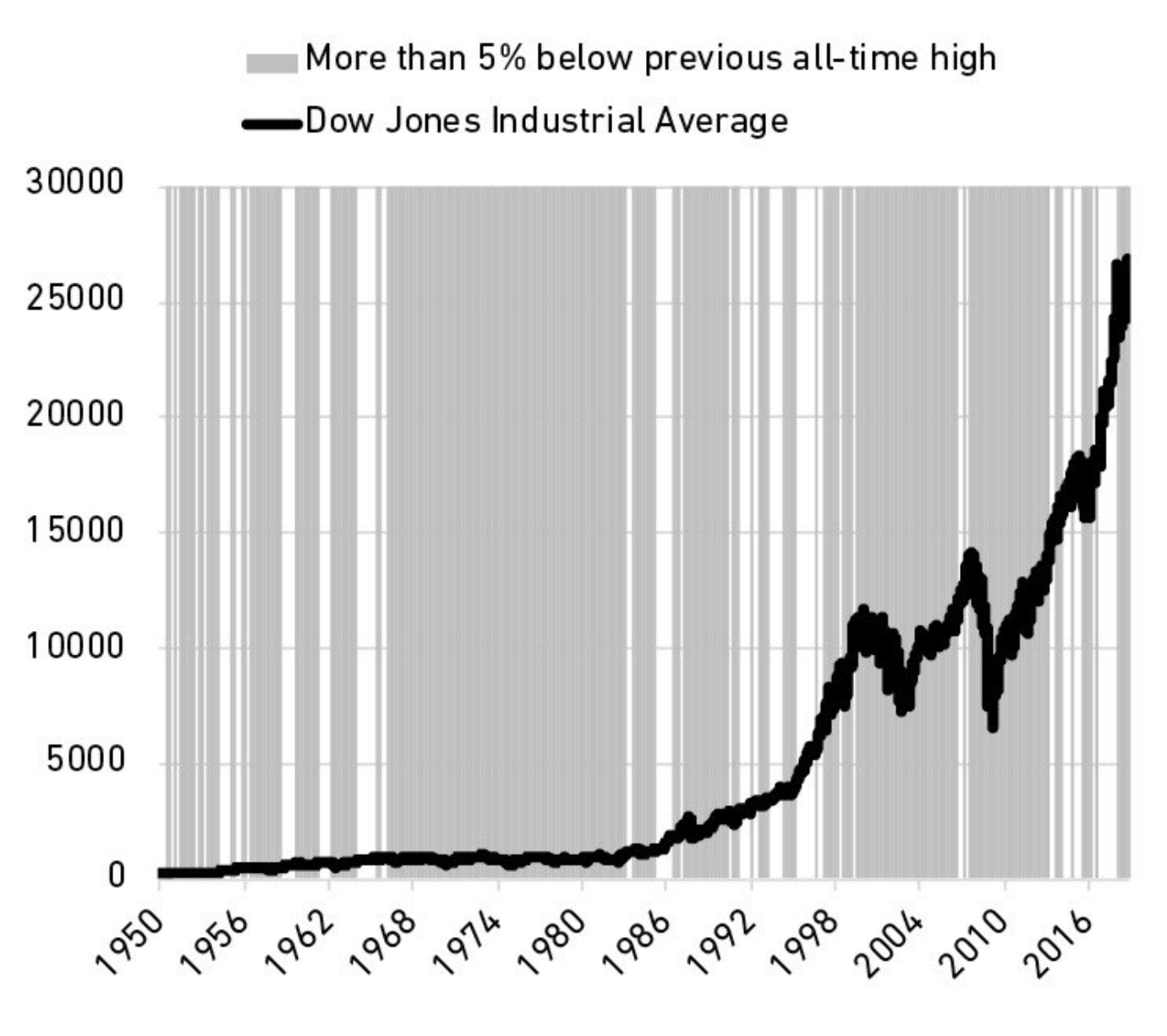

Nothing is as good or bad as it seems on the surface.

Scott Galloway, a professor at New York University, offers an interesting perspective, and it is crucial to remember this when judging one’s own or another’s success: “Nothing is as good or bad as it seems on the surface.”

You are more likely to gain valuable insights only when you seek universal patterns of success and failure. The more universal the pattern, the stronger its applicability to your life.

Posted on 2023/7/29

The longer the remaining health, the better; staying at the table increases the chances of winning.

The key to preventing failure is: having a solid financial plan so that it doesn’t collapse entirely due to one bad investment or an unmet financial goal, ensuring you can continue moving forward on the investment path until the moment good luck arrives.

Chapter 3: Perpetual Dissatisfaction

A considerable portion of readers of this book have found that the money they earn or the wealth they possess at certain points in their lives is enough to meet all reasonable needs in life and allow them to do many things they desire.

Chapter 4: The Mystery of Compound Interest

Warren Buffett’s financial net worth is $84.5 billion, of which $84.2 billion was earned after the age of 50, and $81.5 billion was earned after the age of 65—that much he earned starting from the age when he could begin receiving a pension.

If he had started investing around the age of 30 and retired at 60, few people would know about it.

Buffett treated investing as a career from the age of 10. By the age of 30, he had a net worth of $1 million. Considering inflation, this amount is equivalent to $9.3 million today.

If he were an ordinary person, exploring the world and seeking passion like most people at the age of 10 or 20, how much wealth would he have by the age of 30? Perhaps $25,000?

What if that wealth continued to grow at an excellent annual rate (22%), but he ended his investment career at age 60, starting to spend his time playing golf and spoiling his grandchildren?

How much would his wealth be today?

Not $84.5 billion.

But only $11.9 million.

This figure is 99.9% less than his current net worth.

Chapter 5: Getting Rich vs. Keeping Rich

The fact that “the long-term result is positive, but the short-term process may be terrible” seems counterintuitive at first glance, but many things in life are indeed like this. By the time a person reaches 20, the number of synapses in their brain has shrunk to half of what it was at age 2, because inefficient and redundant neural connections have been cleared, yet clearly, a 20-year-old is much smarter than a 2-year-old. Destruction is a frequent process on the path forward, but it is also an effective way to refine and select the best.

Imagine you are a parent with X-ray vision, able to see inside your child’s brain. Every morning, you would find that the neural synapses in your child’s brain have decreased a little more. You would panic and say, “This is wrong; the synapses are getting fewer. Something must be wrong; we must do something, we need to see a doctor!” But fortunately, you don’t have X-ray vision. What you are seeing is merely the child’s normal process of growth.

The economy, the market, and personal careers usually follow a similar path—a process of continuous growth amidst constant losses.

You need short-term vigilance to allow yourself to survive, so that you can see the long-term optimistic results.

Chapter 7: Freedom

Time freedom is the greatest dividend wealth can bring you.

The highest form of wealth is being able to wake up every morning and say, “Today, I can do anything I want to do.”

If happiness has a common denominator—a universal source of joy—that is complete control over life.

The freedom to do what you want, when you want, and for as long as you want is extremely precious, and this is the greatest dividend that money can bring us.

John D. Rockefeller was one of the most successful businessmen in history. He was also a recluse, spending most of his time alone. He was taciturn, minimizing social interaction; even if you caught his attention, he would remain silent.

A refinery worker who became one of Rockefeller’s confidants once said, “He let everyone speak, while he himself leaned back in his chair, remaining silent.”

When someone asked him why he remained silent in meetings, Rockefeller often quoted a poem to answer:

A wise old owl lives on an oak tree,

The more it sees, the less it speaks,

The less it speaks, the more it listens,

Why can’t we be like this wise old owl?

Chapter 8: The Luxury Car Paradox

There is a paradox here: we all want to use wealth to tell others that we deserve their admiration and respect. But in reality, others often skip the admiration step. This is not because they feel your wealth is unworthy of envy, but because they use your wealth as a benchmark to express their own desire to be admired and respected.

You might think you need an expensive car, a luxury watch, and a big house, but let me tell you, you don’t truly want those things themselves. What you truly want is the respect and envy from others. You think owning expensive things will make others respect and admire you, but unfortunately, they won’t—especially those you hope to gain respect and admiration from.

Chapter 9: The Wealth You Cannot See

A person’s wealth is often invisible because it is the income that has not been spent that becomes wealth. Wealth exists before you make the purchasing decision. Its value lies in the options, flexibility, and growth potential it provides—the ability to buy more things in the future than you can buy today.

Chapter 10: Saving Money

The most effective way to increase wealth is not by raising personal income, but by cultivating your humility.

When you define savings as the difference between your ego and your income, you understand why many people with decent incomes find it difficult to save money. It is because they fight the instinct every day to show off and compare themselves to others who are also showing off.

Chapter 13: Margin of Error

The purpose of the margin of safety is to make prediction unnecessary.

The ability to do what you want, when you want, and for as long as you want is the source of infinite returns.

Chapter 14: People Change

Posted on 2023/7/31

The Advantage of the Golden Mean

When you consider that your ideas will change over time, striving for balance at every node of life becomes a strategy to avoid future regret and maximize the duration of sticking to the plan.

When you consider that your ideas will change over time, striving for balance at every node of life becomes a strategy to avoid future regret and maximize the duration of sticking to the plan.

I have no sunk costs.

In a world where people change over time, sunk costs—unrecoverable expenditures caused by past decisions—are like a roadblock. They make us prisoners of who we were, forcing the future self to act like the past self. This is equivalent to letting a stranger make major life decisions for you.

Chapter 15: There Is No Free Lunch in the World

“Any job looks simple to an observer.”

Volatility is like a fee, not a penalty. Market returns are never free, and they can never be free. They demand a price from you, just like any other product. You are not forced to pay, just as you are not forced to go to Disney World. You could choose a local fair with a $10 ticket, or stay home for free. You might be just as happy, but usually, you get what you pay for. The market is the same. The cost of volatility/uncertainty—the price of obtaining returns—can be called the entry fee, allowing you to gain returns far higher than those offered by low-cost options like cash and bonds.

Chapter 19: Summary

This is because nothing is as good or bad as it seems on the surface. The world is vast and complex. Luck and risk truly exist.

The less vanity, the more wealth. How much you can save depends on the gap between your need for self-expression and your income, and wealth exists precisely in that unseen gap.

Some Reflections

How to Achieve Financial Freedom Through Buying and Selling Stocks

Buffett’s True Secret to Success

- Buffett does not borrow heavily.

- Buffett has endured 14 economic downturns, but none of them made him panic-sell his stocks.

- Buffett never tarnishes his business reputation.

- Buffett never clings to one strategy, one worldview, or one trend; he is always learning and never goes down a single path.

- Buffett does not rely on other people’s money to run the company.

- Buffett hasn’t exhausted himself, hasn’t quit, and hasn’t retired.

Buffett repeatedly emphasizes what is called “Margin of Safety.” His strategy requires that even during a massive bull market, you must always hold some cash. Others might be fully invested and earning a 9% return, but your cash might only yield 1% return. This feeling is difficult, but you must endure this discomfort to ensure that during a bear market, you still have money and are not forced to sell your stocks.

Making money is one thing, keeping wealth is another.

It is foolish to take risks with what you have and need in order to make money you don’t have and need. To make money they didn’t have, and didn’t need the risk what they did have and did need and that’s foolish. It is reasonable to invest a small portion of income without affecting quality of life. But people must be careful of the “Never Enough” impulse, and should not take excessive risks (leverage, shorting stocks, pushing legal boundaries, etc.) to pursue more wealth, but should focus on wealth preservation and slow growth through compounding for sustainable development.

Loving risk can make you money, but it can also make you lose money.

- Earning money requires luck, optimism, and a willingness to take risks.

- Keeping money requires avoiding risk, extreme humility, and fear.

The Straight-A Student vs. The Treasure Hunter

The Straight-A Student

This mindset is like those good students in school who want to get good grades in every subject and fear having any weaknesses. If this person does ten things, they expect to do at least nine well, and they will apologize for the one that wasn’t done well.

But the straight-A student mindset is actually an employee mindset. Everything you do is assigned and must be done. So, if you don’t know what to do right now, or what the consequences of every action will be. If you are an entrepreneur, investor, or leader, this employee mindset won’t cut it.

The Treasure Hunter

Those who invest know that investment portfolios have a strong “tail effect.” Often, most of the projects you invest in will fail, but a few will achieve extreme success, and almost all of your returns will come from those extremely successful projects. This effect is the “80/20 Rule” in investing. Moreover, this “investment” is broad, not limited to stock trading.

The key to the Treasure Hunter mindset is casting a wide net. You estimate there might be gems in this entire mine, so can you say you only explored the spot with gems? Can you say you only bought the pit with gems? You must control the entire area. Football schools, celebrity management, copyright agencies, IP adaptations—all follow this mindset.

We live in a world where “good things” are distributed very unevenly.

- In your lifetime, perhaps only a few books will have the deepest impact on you.

- Perhaps only one or two skills will determine your future.

- Perhaps only a few events will change your destiny.

- Perhaps only a few people are the most important to you.

You must cast a wide net, try many things, and expand your search scope, not fearing the waste of time and money, to ensure you find the best few.

If you only do what is “right” or what history has proven viable, your path will narrow.

Why Ambitious People Live in Disappointment

These are truly “gray” days. You didn’t sell at the last high, and you don’t know when the next high will come. The current point only brings disappointment. These are the days when a top student scores 97 points.

Investing is an activity everyone can participate in, and it provides direct feedback on your decisions. In particular, investing shows you whether you can face the real world.

So, if you are an ambitious person, your life is one of pursuing occasional satisfaction amidst disappointment.